A market economy is an incentive for the development of methods of production and sale of goods. This is facilitated by the desire for personal enrichment on the part of the seller and the chance to buy many goods of different variations - with the buyer. A manufacturer can make money for himself if his product is competitive in the market (he can sell it). The buyer can buy quality goods in the market. Thus, the client and the seller satisfy each other's needs. This article also describes the demand and supply function, the formula of which is very easy to understand.

Supply and demand formula

The purchase and sale process itself is quite multifaceted, in some cases even unpredictable. It is studied by many economists and marketers interested in controlling the flow of finance in the market. To understand the more complex functions that shape a market economy, you need to know several important definitions.

Demand - a product or service that will be exactly sold for a certain price and a certain period of time. If many people want to buy one type of product, then the demand for it is great. In the opposite picture, when, for example, there are few buyers for a service, we can say that there is no demand for it. Of course, these concepts are relative.

Offer - the amount of goods that manufacturers are ready to offer to the buyer.

Demand may be higher than supply or vice versa.

There is a formula for the supply and demand prices, which determines the volume of goods on the market, demand for it, and also helps to establish an economic balance. It looks like this:

QD (P) = QS (P), where Q is the volume of goods, P is the price, D (demand) is demand, S (supply) is supply. This supply and demand formula can help solve many economic problems. For example, if you are going to find out the quantity of goods on the market, how profitable it will be to produce. The volume in the formula of supply and demand, which is multiplied by the price of the goods, is able to solve a huge range of economic problems

The law of supply and demand

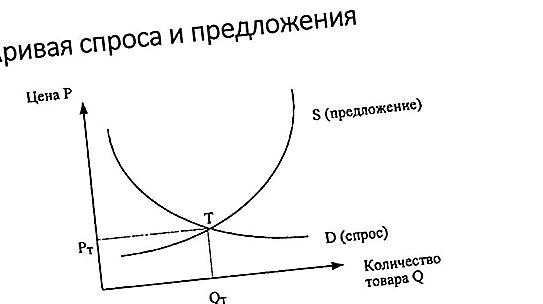

It is easy to guess that between supply and demand there is a connection, which economists have given the name "function of supply and demand", the formula of the function was discussed above. Demand and supply as a picture can be seen on the hyperbole below.

The drawing is divided into two parts - before the intersection of two lines and after it. Line D (demand) in the first part is high in relation to the y axis (price). Line S, on the contrary, is at the bottom. After the intersection of two lines, the situation becomes the opposite.

The figure is quite simple to understand, if taken apart by example. Product A is very cheap in the market, and the consumer really needs it. The low price allows anyone to buy the product, the demand for it is great. And there are few manufacturers of this product, they cannot sell it to everyone, because there are not enough resources. This creates a shortage of goods - demand is more than supply.

Suddenly, after event N, the price of goods jumped sharply. And this means that he has become too expensive for some customers. Demand for goods falls, but supply remains the same. Because of this, there are surpluses that could not be sold. This is called a surplus of goods.

But a feature of a market economy is its self-regulation. If demand exceeds supply, then more manufacturers are moving into this niche in order to satisfy it. If supply exceeds demand, then manufacturers are leaving the niche. The intersection point of the two lines is the level when demand and supply are equal.

Demand elasticity

A market economy is slightly more multifaceted than simple supply and demand lines. At a minimum, it can reflect the elasticity of these two factors.

The elasticity of supply and demand is an indicator of fluctuations in demand, which is caused by price fluctuations for certain goods and services. If the price of a product has fallen, after which demand for it has grown, then this is elasticity.

The formula for the elasticity of supply and demand

The elasticity of supply and demand is expressed in the formula K = Q / P, in which:

K - demand elasticity coefficient

Q - the process of changing the quantity of sale

P - percentage of price change

Products can be of two types: elastic and inelastic. The only difference is the percentage of price and quality. When the rate of change in price exceeds the rate of supply and demand, then such a product is called inelastic. Suppose the price of bread has changed dramatically. It doesn't matter which way. But changes in this industry cannot be so catastrophic as to greatly affect the price tag. But because bread was a commodity in high demand, it will remain so. Price will not greatly affect sales. That is precisely why bread is an example of completely inelastic demand.

Types of elasticity of demand:

- Totally inelastic. Price is changing, but demand is not changing. Examples: bread, salt.

- Inelastic demand. Demand is changing, but not as much as price. Examples: everyday products.

- Demand with a unit coefficient (when the result of the demand elasticity formula is unity). The volume of demand varies in proportion to price. Examples: dishes.

- Elastic demand. Demand changes more than price. Example: luxury goods.

- Absolutely elastic demand. With the smallest change in price, demand changes very much. Such products are currently not available.

Changes in demand may be the result not only of prices for a particular product. If the incomes of the population increase or fall, then this will entail a change in demand. Therefore, the elasticity of demand is better shared. There is a price elasticity of demand, and there is income elasticity.

Elasticity of offer

The elasticity of supply is a change in the quantity of goods offered in response to a change in demand or some other factor. It is formed from the same formula as the elasticity of demand.

Types of supply elasticity

In contrast to demand, supply elasticity is formed by time characteristics. Consider the types of offers:

- Absolutely inelastic offers. A change in price does not affect the quantity of goods offered. It is characteristic for short periods.

- Inelastic proposal. The price of a product changes much more than the quantity of the offered product. Also possible in the short term.

- Offer with unit elasticity.

- Flexible offer. The price of a product changes less than the demand for it. It is characteristic for the long term.

- Absolutely flexible offer. A change in supply is much more than a change in price.

Price elasticity rules

Having figured out what formulas the supply and demand are given, you can get a little deeper into the functioning of the market. Economists have systematized the rules that identify the factors that affect the elasticity of demand. Let's consider them in more detail:

- Substitutes. The more types of the same product on the market, the more flexible it is. This is due to the fact that when prices rise, a brand A product can always be replaced with a brand B product, which is cheaper.

- Necessity. The more necessary the product for the mass consumer, the less flexible it is. This is due to the fact that, despite the price, demand for it will always be high.

- Specific gravity. The more space a product occupies in the structure of consumer spending, the more flexible it is. In order to better understand this point, it is worth paying attention to meat, which is a large cost graph for most consumers. With a change in the price of beef and bread, the demand for beef will change more, because it is a priori more expensive.

- Availability. The less available the product on the market, the less its elasticity. With a shortage of goods, its elasticity will be low. As you know, manufacturers raise prices for what is in short supply, however, it is in demand.

- Saturation. The more a certain product a population has, the more it becomes elastic. Suppose an individual has a car. The purchase of the second is not a priority for him if the first satisfies all his needs.

- Time. Often, sooner or later, substitutes appear in a product, its quantity in the market grows, and so on. This means that it becomes more elastic, as was proved in the paragraphs above.

")