Regardless of where you plan to invest your capital: in a friend’s enterprise or in your own life, you need to clearly calculate the money that you will receive in the future. To this end, there is a concept called financiers "compound interest." Of course, there are a large number of online compound interest calculators. However, in order not to get into a puddle, it is better to understand the methodology for calculating this indicator yourself. In order to help you with this, this article was written.

Theory of the value of money in time

According to one of the many economic concepts, money tends to depreciate over time. Today's contribution, which costs, say, $ 1000, will cease to cost the same in 5-6 years.

But the value of money is affected not only by the time period. There are three main factors that can affect the real value of cash capital:

- time;

- inflation;

- risk.

Given that investing in itself involves making a profit in the future, there is a need to calculate what it will be after the allotted time period. After all, when an investor invests in a certain enterprise, he must feel the difference between what he invested and what he gets. For this, two basic concepts of contribution are introduced: the current and future value of cash capital.

Current value of money

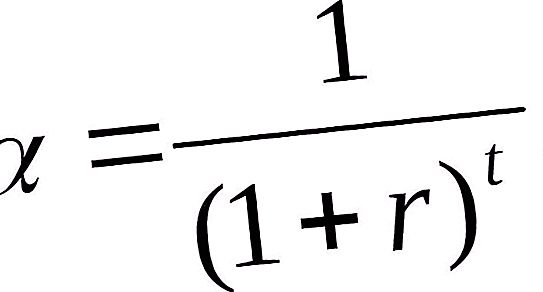

The invested current value of the money supply is future financial income that is reduced to the current time period taking into account the established interest rate. Establishing the current value of money is characterized by a process called discounting. Being the opposite of building, it helps to establish how much money needs to be invested today in order to receive $ 10, 000 in 6 years.

This simple arithmetic operation is performed by multiplying the upcoming cash flows by a discount factor.

Where: α-discount factor; r is the discount rate divided by 100%; t - serial number of the year for which the calculation is made.

Future value of capital

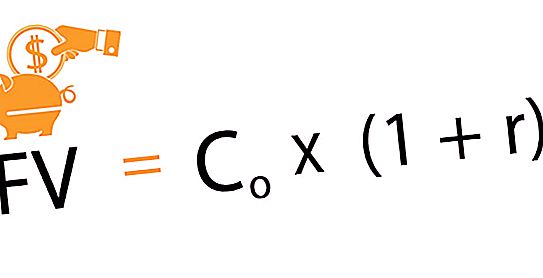

The future value of the unit of investment is the amount that results from investing on the current date of the nth amount of money after the agreed amount of time and a certain interest rate. This method of calculating future earnings is called “build-up”. This is a movement from the present to the future. When taking into account the agreed rate from year to year, there is a gradual increase in initial investments. Thus, the first capital investment increases its value over time. When considering investment projects, the interest rate plays the role of the profitability ratio of operations.

The following formula is used to determine future earnings for investments made today.

Where: Co - initial investment; r is the interest rate; n is the agreed investment period.

It was the accumulation method that led to the emergence of compound interest.

What is a compound interest?

Let's imagine that you invested at 12% per annum 200, 000 rubles. For the first year, your profit will be 24, 000 rubles: 200, 000 + 200, 000 * 12% = 224, 000 rubles. However, you, according to the agreement, do not take this money, but they are transferred to the category of deposit and in the second year the interest is calculated not on 200, 000 rubles, but on 224, 000 rubles, etc.

Such a scheme, in which interest is accrued on the profit in the previous period, is called compound interest or capitalization.

This method works both for deposits and loans, if you do not plan to return money to the bank in the first few years. Moreover, according to the agreement, interest is calculated either every month, or quarterly, or once a year.

Compound interest functions

When conducting a variety of financial calculations, one often has to resort to solving problems of creating a cash flow with available characteristics and identifying their value. To simplify the calculations, standardize them, use the derived functions of compound interest, which display the dynamics of changes in the cost of capital investments over the allotted time period.

There are 6 such functions in total:

- The amount of future savings, taking into account the compound interest rate.

- Annuity future value or accumulation of a unit for the period.

- The current value of the annuity.

- Compensation Fund Factor.

- Partial payment for depreciation of a unit.

- The reversal factor or the current value of the unit.

Volume of future savings taking into account compound interest rate

This function of compound interest was considered by us above when it came to the future cost of capital and growth. When determining future earnings, the following are taken as the basis: initial investment, compound loan rate and the period for which investment is provided.

Future Annuity Value

Allows you to determine the increase in the savings account, which involves regular contributions of the depositor, for which a percentage is charged at a specified time interval.

It is calculated by the following formula:

FVA = M * ((1 + r) n - 1 / r, where: FVA - the future price of money; M - the amount of constant payment; r - loan rate; n is the time period.

Thus, if you pay 1, 500 rubles each month, for three years at a rate of 15%, then based on the results of all payments, your future cost of standing payments will be 67, 673 rubles.

Regular equal contributions

The compensation fund factor shows the amount of the contribution that must be made on a regular basis in order to obtain the planned amount by the compound interest at the end of the set period.

To calculate, you must use the formula:

M = FVA * r / ((1 + r) n - 1).

Like all formulas related to the calculation of cash flows, this is easily derived from the previous one.

If you plan to buy an apartment after 6 years, the cost of which is, roughly speaking, $ 1, 000, 000, then at a fixed annual interest rate of 15%, you need to pay $ 8, 645 a month to the bank.

Reversion factor

This compound interest function is the inverse of the first. The calculation is carried out according to the following formula:

PV = FV / (1 + r) n, where: PV is the initial contribution; FV - Future Admission; r- interest rate; n is the number of years (months).

This function gives an idea of how much you need to invest today in order to get a guaranteed profit under the given conditions (period and percentage).

For example, the current value of 20, 000 rubles, expected to be received after 4 years at an annual rate of 15%, will be 11, 435 rubles.

Fair value of a regular annuity

Demonstrates the cost of regular payments to date. The first receipts are expected at the end of the first year, month, quarter, and subsequent - at the end of each subsequent time interval.

The formula for the calculation is as follows:

PVA = M * (1 - (1 + r) -n) / r.

A simple example where this technique is used can be a situation in which it is necessary to establish the size of a loan given for a certain period of time, at specified interest rates and monthly payments to the bank.

. What are the first spring mushrooms called?")