Cashless payments are, figuratively speaking, the vessels of the economy. They are made by making payments on bank accounts and are regulated by the Civil Code of the Russian Federation (chap. 45 and 46), the Regulation on non-cash payments of the Central Bank of Russia No. 2-P dated 04/12/2001. Money is transferred from the payer's bank account to the seller’s bank account (recipient).

The transformation of non-cash payments into the main payment instrument indicates a certain level of economic development. In developed countries, cash turnover is about 5% of the total cash flow. Cashless payments allow the Central Bank to control the cash flow of the Russian Federation. With their help, money circulation is significantly accelerated, temporarily free cash is formed, and with their help the banking system increases its ability to lend. Also, as a result of the acceleration of money circulation (and consonant with Marx's “chain-Commodity-Money-Commodity” chain), material circulation in the state is also accelerating.

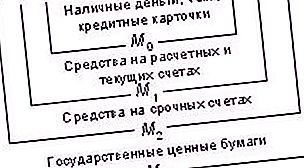

Aggregate structure of monetary circulation

As you know, since 1992, cashless payments in Russia have been analyzed and administered using the Bank of Russia accounting for monetary aggregates, in which different types of money are grouped differently. What is their economic content, you can see in figure 1.

Scheme 1. Aggregate structure of monetary circulation

The unit M 0, according to the classical theory, combines cash, money on card accounts, electronic money and checks, that is, the most highly liquid assets. These are assets that individuals are actively using. The formula by which it is determined has the following form: M0 = C + checks (1).

The augmented nature of the aggregate M 1 relative to M0 is displayed by the formula 2: M 1 = M 0 + money on current and settlement accounts in banks (2).

This unit also displays the economic activities of legal entities, accumulating funds in current and settlement accounts and using them for business activities.

The unit M 2, in turn, is supplemented to the unit M 1. It includes funds of an urgent nature, i.e., a deposit of securities and deposits. Thus, it represents the long-term liabilities of the banking system.

Cash is the main payment instrument

For the classical aggregate model of money circulation, cashless payments are aggregates M 1 and M 2.

Moreover, according to the statement of the First Deputy Chairman of the Central Bank Georgy Ivanovich Luntovsky, currently the main payment instrument for Russia is still cash. True, their share in the M2 unit decreased from 35.2% in 2005 to 23.8% (information at the end of 2012.)

The organization of their turnover is expensive: special cash equipment, a collection system, etc. are required. At the same time, for Western countries this role is mainly played by cashless payments. Cash significantly reduces the speed of money turnover - one of the factors of a dynamic economy.

Correspondent Account Mechanism

Cashless payments are one of the functions of a bank. For their implementation, it is not enough to open bank accounts with self-supporting enterprises and current accounts with budget-financed organizations. A mechanism for bank correspondent accounts is also needed. How does this system work?

Imagine a typical situation: enterprise A buys the products of enterprise B and pays for it non-cash. How is this opportunity realized? With the help of mutual settlements between the buyer's bank (B-A) and the seller's bank (B-B), i.e., financial institutions where the enterprises under consideration opened their current accounts. Obviously, the buyer’s bank must transfer from his account the corresponding non-cash funds to the seller’s bank to his account. To do this, both banks open their correspondent accounts with the Central Bank of Russia (CBR): COP. Thus, cashless payments are financial services provided by banks to customers' business activities using correspondent accounts. Let us return to our situation, both correspondent accounts of both Bank A-B and Bank B-B are opened in the same institution - the CBR (respectively: KS-BA and KS-BB).

How does the non-cash payment system organized by the CBR work? In three stages.

- First. Entity A transfers the funds in the amount of the transaction from its current account to the correspondent account B-A, entrusting payment to its counterpart B.

- Second. According to the payment document of enterprise A, his bank BA instructs the Central Bank to write off the corresponding amount from the correspondent account of KS-BA to the correspondent account of the bank serving the seller of KS-BB.

- Third. Bank B, tracking the receipts to its correspondent account KS-B, notices the received payment amount to the address of its client B and transfers it to its current account. Such non-cash payment constitutes the financial basis of the economic turnover.

For a bank, a correspondent account has a double structure - external (NOSTRO opened with the Central Bank) and internal (LORO - internal offsetting account). The balances on the NOSTRO account and on the internal offsetting account mirror each other. To ensure this, both parts of the correspondent account are constantly checked against each other.

Settlements by payment orders

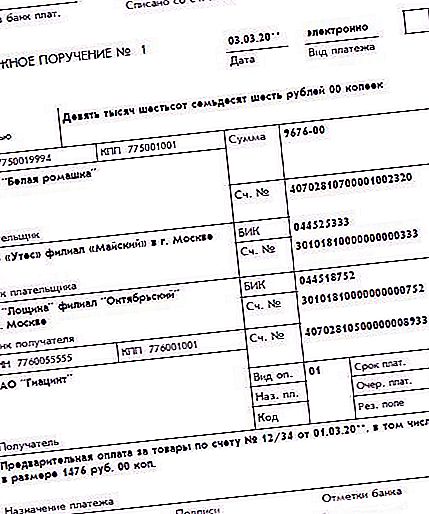

Most often, cashless payments are initiated by the payer organization. She turns to the bank serving her bank account with a documentary request - to transfer funds from him to the bank account of their recipient. The document displaying this appeal is called a payment order. You can see a sample of it in the figure below.

By means of payment orders, non-cash payments are made in the areas of transferring funds to the budget and extra-budgetary funds; settlements of counterparties in the course of their business activities; credit and deposit banking transactions; other non-cash transactions.

Normative documents on cashless payments

The form of this document and the rules for filling it out are determined by the Regulation of the Central Bank No. 2-p dated 03.10.2002 and its Instructions No. 1256-U dated 03.03.2003 (other types of cashless payments are also administered by these documents).

It is signed by the financially responsible persons of the payer organization, as a rule, this is the director (chief) and chief accountant. The instructively determined period of validity is 10 days, not counting the day itself when the payment order is issued. The sample shown in the figure should be supplemented with the above signatures, as well as the seal of the paying organization. The latter is obliged to take into account its payment orders in a special journal

Cashless payments of organizations (enterprises)

The organization of cashless payments in the organization (at the enterprise) serves the sphere of economic relations of these legal entities. By cashless transfer, the company receives revenue from the sale of its finished products (services rendered), and the organization receives financing for the performance of its functions. These funds are transferred to the settlement account of an enterprise or organization in most cases by payment orders. The proceeds received are partially spent on settlements with suppliers. There is a payment of taxes and mandatory payments to non-budget funds. At the same time, payments are made as part of the balance of funds in the current account of the enterprise (organization) or within the framework of a bank loan.

However, there are certain patterns in making such payments.

The principles of organization of non-cash payments by enterprises (organizations)

The organization of cashless payments in the organization (at the enterprise) is guided by certain principles:

- The funds are stored in the bank accounts of the enterprise (organization).

- Enterprises (organizations) are free to choose both the servicing bank and the form of cashless payments.

- Opening current accounts of an enterprise (organization) is controlled by the tax authority.

- The basis for writing off funds is the order of its owner.

- Payment to suppliers is close to the time of shipment of goods, raw materials.

Payment Priority

Cashless payments in the event of a shortage of funds in the current account of an organization (enterprise) are made in a strictly established manner regulated by Art. 855 of the Civil Code of the Russian Federation.

First of all, payments are made on writ of execution for harm to health, as well as for the transfer of alimony. The second - on the writ of execution relating to severance pay, payments to authors for intellectual activity. The third stage includes payments for labor remuneration, transfer of taxes (fees), insurance payments to the budget. By the fourth - on the rest of the writ of execution. In the fifth turn - for the rest of the payment documents. The procedure for cashless payments is controlled by banks. In case of violation, in accordance with the procedure established by Art. 866 of the Civil Code of the Russian Federation, a bank that negligently performed the control function pays interest according to Art. 395 of the Civil Code of the Russian Federation.

Traditional forms of payment documents

For non-cash settlements, except for payment orders, business entities of the Russian Federation use others: letters of credit, collection orders, electronic payments, payment requirements - orders, checks.

The letter of credit form is convenient for the seller, i.e., the person in whose favor the letter of credit is opened. The client-buyer applies to his bank with an order - to issue a letter of credit. For this purpose, form 0401063 is used. The Bank, on the basis of the instruction, is obligated to act as a surety for payment for the installed goods delivered in accordance with the agreed documents. The amount of payments and the time period for their implementation is specified in the order. Thus, the seller of the goods receives a guaranteed payment: either at the expense of the buyer, or at the expense of the bank loan he received. The issuing bank contacts the supplier's bank (executive bank). Money is transferred from the buyer's account to the letter of credit of the executive bank, the latter credits it to the supplier.

Checks are issued by the tank to the check holder, and use them to pay cash to the drawers immediately after presenting the check.

In case of collection non-cash payments, their initiator is the supplier. He instructs his bank to receive the funds transferred by the payer and credit them to his current account.

Electronic payment systems

The 21st century has given us a progressive method of calculation - electronic payments. The implementation of cashless payments has become more affordable. A client can transfer funds from his payment card or from an “electronic wallet” type account opened in an electronic payment system at any time of the day to another account or card. This makes it possible to make payments at any time of the day, from your PC, including in a comfortable home environment.

To do this, the WM Keeper Light WEB application is installed on the PC, and Telepat is installed on the smartphone.

Now Russian users use the services of several dozen payment systems. In 1998, the PayCash system appeared, in 1999 - WebMoney, in 2002 - Yandex.Money. These payment systems perfectly interact with the international card payment systems MastercardMass and VisaInternational. The activities of electronic money systems are regulated by the Federal Law of the Russian Federation “On the National Payment System”.