Profitability of a business is a necessary condition for its existence. It depends on many factors, the consideration of which is necessary for decision-making. What should be the volume of production? What are the acceptable costs? At what prices will the products be competitive and in demand on the market?

What is the breakeven point. Simple definition

The initial stage of any financial activity is knowingly unprofitable. The costs of raw materials or the purchase of goods, the maintenance of storage facilities, wages to employees must be incurred before the profit begins to flow.

You can’t count on revenue before the mass of sales exceeds a certain critical threshold. In the best case, at first only some costs will be compensated, but the overall result will be unprofitable.

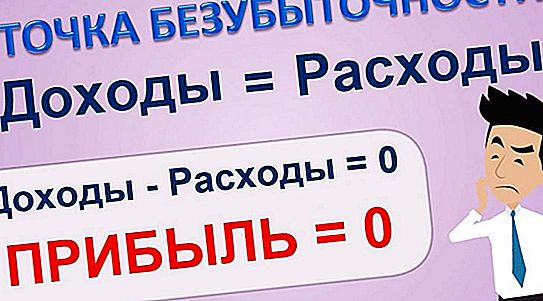

It makes no sense to talk about profit at the breakeven point. It is zero.

The sales volume that balances the cost of selling products with revenue is called the breakeven point (TB). Only the achievement of self-sufficiency gives a guarantee of subsequent profit.

What determines and what gives TB

Sales volume is a determining, but not the only factor in its existence. Fixed and variable costs (costs) are the threshold, the achievement of which allows us to say that the loss-making of the initial stage has been overcome.

The size and nature of revenue also has an impact on reaching the breakeven point of production. Accounting for all the dependencies allows the entrepreneur to draw conclusions:

- about the possible profitability of the planned business;

- about problems when choosing one or another way to achieve TB;

- on linking the volume of sales with pricing policy;

- the existence of options for implementing the goals.

You can relate to the breakeven point as a face in the level of sales, followed by profit, or as the end of a period of non-profit operation. The essence of this does not change. The main thing is to determine it as close to reality as possible.

Success formula

Before you turn on the calculator, you need to firmly understand the difference between fixed and variable costs. The former do not depend on the volume of goods and services sold, while the latter proportionally change after it.

For example, the cost of heating premises or repairing equipment will remain the same with an increase in sales, and with their decrease. And salary, energy or components transfer their value to the final product directly.

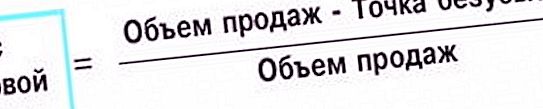

If we designate sales revenue as VP, the difference between revenue and variable costs as RVP, and fixed costs by the acronym PZ, then the formula for determining the break-even point will take the following form:

TB = VP * PZ \ RVP.

Why is that? Consider the ratio of fixed costs to the difference between revenue and variable costs. The difference itself is nothing more than a profit from the sale. Hence, the whole ratio is a certain coefficient that changes the amount of revenue in such a way that it appears as a breakeven point.

Not everything is clear?

Imagine that the coefficient is equal to one. Then TB in monetary terms will be equal to all revenue. That is, with such costs and revenues, this is the desired point. By changing the ratio of costs and revenue, we can choose a sales volume that allows opportunities and that meets the wishes.

How to calculate the breakeven point is shown in the table.

| Data | Business projects | Total | ||

| A | IN | WITH | ||

| Volume of sales | 2, 500 | 1, 500 | 1, 600 | 5, 600 |

| Variable costs | 1 900 | 1, 280 | 1, 380 | 4, 560 |

| Fixed costs | 800 | 800 | ||

| Profit | 240 | |||

In the example, the company is analyzed, which initiated three projects, A, B, C. In total, the company made a profit of 240 thousand rubles. This means that the breakeven point has already been passed.

Important! The data for the projects for which the calculation is carried out must relate to the same period.

Since in ruble terms our point is the revenue at which the losses cease, it is clear that the smaller the value it takes, the better the businessman, the less he has to wait until the project begins to pay for itself.

Not a single point. Something is missing here

It would seem that the position of the company on the market can be uniquely determined by the breakeven point. The company is the more firmly standing on its feet, the less revenue required for profitable work. And there is. But only in the case when projects and objects of analysis of approximately equal value are compared.

In the shoe shop, where the shoemaker himself and his assistant work, the break-even point may be several thousand rubles. And for a small grocery store, several thousand are no longer money. What can we say about large companies and corporations?

Their breakeven may start with millions and billions, but this does not mean at all that their situation is as much worse than in a shoe shop. What is missing in the wording, what is the breakeven point so that it can serve to compare different representatives of the business community?

Size matters

It is obvious that a corporation with trade around the world is much stronger on its feet than a small enterprise. But TB believes this is not the case. You can rely not on the amount, but on its share in the total turnover. Then it turns out that giants are much stronger than dwarfs, as it is in reality.

The formula used to calculate financial strength is very similar to the TB formula. Sometimes they are called sisters. The same actors participate in them: revenue from sales, variable and fixed costs of the breakeven point. It is called the safety factor (ZP) and looks like this:

GP = (VP - TB) VP.

Here we are talking about the share of revenue remaining after deducting the break-even amount in the total amount of money received. It is no coincidence that it is called a safety factor. The larger the share of money abroad, the stronger the market position.

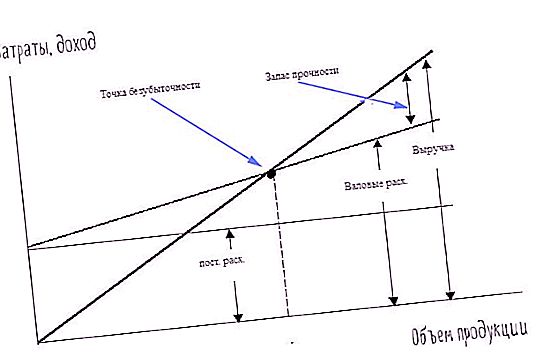

Better than formula

There is a method for determining TB in which all of the above is presented in visual form. This is a graph. It is built on the values of the same formula or function, expressed mathematically. Therefore, the data for its construction are already listed above:

break-even point volume;

fixed and variable costs.

To plot a graph, two axes are needed: abscissa and ordinate. The first is located horizontally. We put off the sales volume on it. The second, vertical, is used to indicate costs.

The inclined line passing through the origin is the revenue graph, horizontal - fixed costs, the second inclined - variables. The intersection of revenue and total cost schedules is the breakeven point. Gross costs, that is, the sum of fixed and variable costs of the breakeven point is expressed by raising the line of variable costs by the amount of fixed.

You can clearly see how profit is growing relative to gross expenditures, as well as safety margin. Different forms of presentation of information complement each other and provide a better understanding of the formation of economic indicators.

Important! The breakeven point can be expressed in sum, quantity or percentage. The choice of one or another method depends on the circumstances and tasks of analytics.

Deepening analysis

All formulas and graphs built on their basis give quite satisfactory accuracy when it comes to one product. But what if several projects are launched, as it often happens in life?

If you put down in one revenue and expenses from different industries, the overall picture will be drawn correctly. But behind the facade of the total well-being of all projects, those may be hiding that either do not give an estimated profit or form losses. The question arises: how to evaluate each contribution to the common cause individually?

That is, the question of what is the breakeven point, we are talking about the calculation separately for each component of production or trade. If the components of revenue are mostly known, then it is difficult to share costs, especially fixed ones. Usually they do this: all expenses are divided by project in proportion to revenue.

As usual - doesn't mean right

But here the analyst again treads on the same rake: puts together in one heap what should lie separately. This problem is solved by the expansion of fixed costs for each range of products. For example, one workshop is used to make pencils, and fountain pens are made in another workshop.

Depreciation, electricity, heat costs in this case can be calculated separately. With the remaining part of the costs that cannot be distributed, they proceed as indicated above: they are divided in proportion to the revenue from the products.

Analysis of the components is more accurate and contributes to the adoption of the right management decisions. But it is more complicated. Instead of one or two formulas, it is necessary to apply the number of calculations, which will be a multiple of the analyzed factors. The same applies to graphs. Instead of straight lines, curves appear that combine the data of individual segments.

Applicability Conditions

There are a number of circumstances in order for the break-even point calculation and subsequent analysis to be effective and contribute to the economic growth of the company:

- regularity;

- calculation for the enterprise as a whole and for individual projects;

- stability of functioning;

- sufficiency of finance.

Each of the points is quite simple and does not require detailed explanations. What is the breakeven point? The type of analysis to be performed during periods of credential occurrence, for example, every month, quarter, or year. Gaps significantly reduce the reliability of the information.

When an enterprise is in a fever during times of reorganization and change, no analysis can be accurate. Adequacy of finance is necessary to reliably cover all needs and payments. Lack of money leads to stability violations, the negative impact of which was noted above.

: biography, creative activity and family")