The market is a competitive form linking business entities. The market mechanism is the mechanism of mutual relations and actions of the main elements of the market, which include demand, supply, price, competition, the main elements of market laws. The market mechanism satisfies only those needs of society that are expressed through demand. The interaction of market demand and market supply is the main component of the relationship between buyers and sellers, as well as between consumers and producers.

What is demand?

Demand is the solvent demand for a certain product or service.

The amount of demand is the number of products, as well as services that customers are willing to purchase in a given period of time, in a given place and at set prices.

The need for any good implies a desire to possess the goods. Demand implies not only this desire, but also the opportunity to purchase at prices that are set on the market.

Types of supply and demand:

- market;

- individual;

- industrial;

- consumer.

Demand and supply for goods are determined by many factors, both price and non-price. Consider them all.

Factors that influence demand:

- advertising;

- product availability;

- the usefulness of the goods;

- fashion and taste preferences;

- consumer expectations;

- amount of income;

- natural conditions;

- political situation in the state;

- change in preferences;

- the price that is set for interchangeable products;

- number of population.

The demand price is the highest possible price a buyer can pay for a product or a service provided.

Demand can be exogenous and endogenous. The first is that type of demand, which is influenced by external factors or government intervention. Endogenous is also called internal demand, its feature is that it is formed within society.

Demand is a request for existing or potential buyers, as well as a group of consumers of products in accordance with their monetary capabilities for a particular purchase. The need for certain products is a reflection of market demand.

The nature of the law of demand is simple. In other words, the higher the price of the product, the less consumers can afford, and vice versa (based on the same amount of money). However, in practice, everything is a little more complicated: firstly, the buyer can replace the goods (this is called substitute goods), and secondly, he can add money to buy a certain number of products.

Law of demand

The law of supply and demand is an economic law that establishes how much the volume of demand and the volume of supply of products depend on their prices. Alfred Marshall finally formulated this law in 1890.

When the price of a certain product rises, but other parameters remain the same as before, then demand will begin to be presented for a smaller number of products.

The interaction of supply and demand in the market sets product prices.

Elasticity of demand - what is it?

This concept denotes an indicator that expresses fluctuations in demand in the aggregate. These fluctuations are often caused by changes in pricing policies for a product or service. Elastic demand is one that has formed under the condition that the change in volume (in percentage terms) exceeds the decrease in prices.

In the event that the indicator of price reduction and increase in demand (also in percent) are the same, in other words, the growth in demand is only able to compensate for the fall in prices, elasticity is equal to one.

In another case, if the price drop exceeds the volume of demand, then the demand is inelastic.

The conclusion follows: demand elasticity is an economic term that characterizes the consumer’s sensitivity to changes in product prices. This phenomenon also depends on the income of the population. Hence the classification of elasticity: by price and by income.

The reaction of customers to price variability is strong, neutral and weak, each of which creates a separate type of demand: elastic, inelastic and completely inelastic.

There are a number of products with different elasticities at a price. Products such as bread and salt are the best examples of inelastic demand. Here, neither an increase nor a decrease in prices for this product affects the number of consumers.

Sellers and manufacturers use the concept of elasticity for their own purposes. If the indicator is high enough, then they are going to a sharp decline in prices in order to increase sales. Accordingly, they receive more profit than if prices were higher.

For products with a low level of elasticity, it is impossible to go for lower prices and increase production. In this case, there is no economic benefit.

When there are a large number of sellers on the market, the demand for any product is elastic. Therefore, in the event of a price increase from some, buyers purchase goods from others.

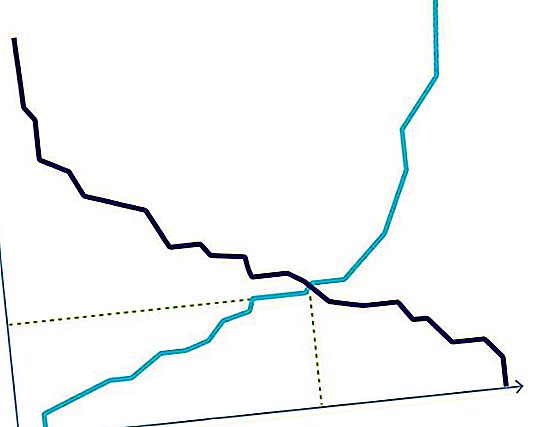

Demand curve

The demand curve is created in order to show the amount of products that can be sold for a given time at a given price. The higher the level of elasticity of demand, the higher the price can be.

The demand curve is a graph that illustrates the relationship between the number of consumers wishing to purchase a product and the price set on it.

The demand curve is depicted in total for all buyers, but taking into account each separately. Sometimes this graph is presented not in the form of a curve, but, for example, in the form of straight lines. It depends on the market situation.

Often, the demand curve is considered in conjunction with the supply curve: this gives a complete picture. The chart is able to fully characterize the market situation. The supply and demand curve at the intersection gives the market an equilibrium price. This, in turn, regulates and stabilizes the relationship between sellers and buyers.

What is an offer?

The interaction of supply and demand is an integral process of the economy, which is characteristic of all developing countries of the world.

It is impossible to objectively analyze the market mechanism without an offer. It characterizes the economic situation in the market on the part of sellers, not buyers.

A proposal is a set of products and services on the market that are sold at a given price.

The value of the proposal is the number of products, services that sellers are currently offering at a given price, but the value of the offer is not always equal to the volume of production or the volume of sales.

The offer price is the approximate minimum price at which the seller is ready to give his goods.

The economic situation in the market can be characterized by the volume and structure of supply. They also affect production and pricing. All products that are on the shelves of sellers, and even those that are still on the way, belong to the product offer.

Supply volume is directly related to the price. In the event that the price turns out to be low, a smaller part of the goods is sold (most remain in warehouses), but if the price reaches the maximum level, then much more products appear. In this case, even defective goods are used.

There are three intervals over which the proposal is examined. Up to a year - short-term, from one to five - medium-term, and more than five years - long-term.

The volume of supply is the quantity of goods that sellers want to sell per unit of time.

The law of supply looks like this: the volume of goods increases with rising prices and also decreases if the price decreases.

The change in supply and demand is due to many factors. First of all, it is a change in prices for a given product or one that can be replaced. Also influenced by the volume and cost of production.

Supply, like demand, has non-price factors. These include:

- the appearance on the market of new firms;

- natural disasters;

- wars or other political actions;

- production costs;

- projected economic expectations;

- change in market prices;

- production modernization.

Technological progress is having a huge impact. It reduces production costs, speeds up and simplifies work.

An offer is an economic phenomenon in which a seller wishes to sell his goods on the market at set prices. It, as well as demand, is influenced by many price and non-price factors. Among them:

- presence on the market of substitute products;

- complementary goods (complementary);

- new technologies;

- taxes and subsidies;

- amount of resources used;

- availability of raw materials;

- natural conditions;

- market size;

- waiting for goods / services.

Law of supply

The volume of supply increases with product prices. This law is only valid if, along with prices, the volume of production of goods increases and the seller (producer) begins to receive more profit. The real economic picture is more complicated, but these trends are inherent in it.

Supply determines demand, and demand determines supply. So Karl Marx thought. To date, his theory is also relevant. The offer is able to generate demand due to the range of products and prices that are set on it. In turn, demand determines the volume and structure of product supply. This happens because the products that are consumed the most are used.

The process in which such a price is set for a given product that can satisfy both the buyer and the seller is the interaction of supply and demand.

Elasticity of offer

This is an indicator that reproduces the supply changes in the aggregate that occur due to price increases. In the event that the increase in supply is greater than the increase in prices, then it is characterized as elastic (the elasticity of supply is higher than unity). If the increase in supply is equal to the increase in prices, then the offer is called single, respectively, the indicators are the same. And also, if the increase in supply is less than the increase in prices, then in this case the offer is inelastic (the elasticity of the supply is less than one).

Whether the proposal is flexible or vice versa depends on several factors:

- product manufacturing features;

- the duration of its storage;

- time spent on manufacturing;

- hourly factor.

The interaction of supply and demand helps to establish a suitable price for the product, thereby determining the relationship between the consumer and the manufacturer.

Offer may change:

- market prices (in particular, substitute goods);

- taxes

- cost of production;

- consumer tastes;

- scientific and technical achievements;

- number of producers;

- manufacturers' expectations.

The interaction of market demand and market supply is a process in which an equilibrium price is established that satisfies both buyers and sellers.

Supply curve

The supply curve characterizes the quantity of goods that are sold at different prices, but at a given time.

The supply schedule depicts the ratio of market prices to the amount of products that manufacturers offer. This curve is most affected by production costs. This allows us to produce more products to increase profits. Another factor that affects the supply schedule is technological and scientific progress. Advanced production technologies allow you to work faster and spend less raw materials, as well as human resources.

A supply and demand schedule is needed in order to fully depict the market situation. It helps to understand pricing policy, establish the necessary volume of production and draw up a profitable plan for manufacturers and sellers.

In order to represent the equation of supply and demand, linear functions are needed. You need to know two points in order to build them. To find them, a supply and demand curve is depicted, their dependence on price and quantity of products. The point at the intersection of the graphs is the solution. It is commonly called the equilibrium point.

The interaction of market demand and market supply is an economic process that generates the formation of a market price that satisfies the buyer and seller.

Factors of supply and demand are those that affect their value. The main for both indicators is the price of the goods. However, there are other non-price factors.

Market equilibrium is a phenomenon in which indicators such as supply / demand have the same level. The equilibrium price is the price at which the magnitude of these indicators is the same. In other words, the price at which the manufacturer offers a certain amount of goods, and buyers buy all of it. This phenomenon in the economy is extremely rare, and at this time supply is equal to demand.

How was the law realized?

For the first time in the fourteenth century, the theme of the interaction of supply and demand was raised. The Muslim historian, as well as the philosopher and social thinker from the Arab countries came to the conclusion that the more exclusive the product, which is also in great demand, the higher the price for it. The name of this philosopher was Ibn Khaldun, it was he who became the founder of the law on supply and demand.

Further, his idea was developed in the sixteenth century in the writings of the Spanish economist Juan de Mathienzo. He described the theory of subjective value of goods, which leads to a distinction between the concepts of supply and demand. He also introduced the concept of "competition" to describe trading and market rivalry. In his numerous works, several factors are identified that influence pricing.