In attempts to create an idea of economic reality, experts began to use simplified theories. They are called macroeconomic models in a different way. This concept should be understood as a form of description of processes and phenomena in order to find a close connection between them.

The Importance of Macroeconomic Models

They are an abstract reflection of the real economic picture. This is due to the fact that during the study it is impossible to immediately take into account the diversity of the available details.

Therefore, no model can be called perfect and complete. It does not provide the only correct answer sent to a certain state in a certain time period.

However, using models, governments can:

- To analyze such macroeconomic phenomena and processes as inflation, unemployment, interest rates, exchange rates and much more.

- Make forecasts of macroeconomic processes and phenomena.

- Find solutions to problems.

The use of macroeconomic models allows the optimal combination of monetary, fiscal, foreign exchange and foreign trade policy instruments. This is necessary in order to smooth out the economic cycle and cope with crises.

Varieties of models

Depending on what tasks are investigated, different types of models are used. The classification is based on several criteria:

- According to the method of presenting the process or phenomenon under study - graphic and economic-mathematical.

- By duration - short-term and long-term.

- In terms of coverage of the foreign sector - closed and open. Closed models do not take into account the influence of other countries; open models take into account the impact of the outside world on the national economy.

- By the number of economic entities - simple (firms and enterprises, households) and complete (state participation).

- By type of reflection of events in time - static and dynamic. The former do not take into account the time factor, which is necessary for the commission of an event. The second characterize the relationship of changes in economic indicators over time.

The most famous models of macroeconomics

In the course of historical development, a huge number of them developed. But among them can be called those macroeconomic models that have gained great popularity.

The model of circular flows.

It says that real and cash flows are realized freely when the total volume of production equals the total costs of firms, households, states and the rest of the world.

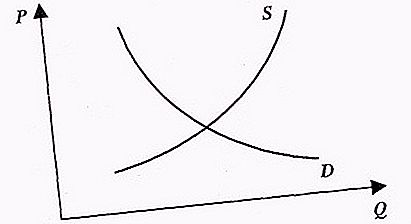

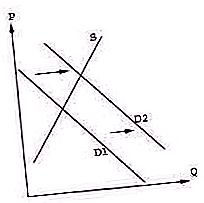

Aggregate demand and aggregate supply model. It allows you to:

- identify the conditions under which equilibrium is achieved in macroeconomics;

- determine the necessary level of output and price level;

- identify the reason for the change in the equilibrium volume of production and the price level, and also show the consequences of these changes;

- present options for economic decisions.

Phillips and Laffer Curves. The Philips curve indicates the relationship between unemployment and inflation.

The Laffer curve is a graphic representation of the Laffer effect. Its essence is that lowering tax rates will lead to a reduction in government revenues in the short term. In the long run - to increase investment, employment and increase the level of savings.

Solow Economic Growth Model.

Thanks to it, it is possible to determine the optimal saving rate at which the maximum possible consumption is ensured.

When constructing macroeconomic models, two types of variables are used.

The concept of exogenous variables

By the time models are built, they are already known. Exogenous are variables that are set externally and considered external. In other words, this is background information.

As such variables are, as a rule, the fiscal policy of the state, the monetary policy of the national bank, as well as their tools:

- the amount of money supply;

- reservation rates;

- tax rate;

- refinancing rate;

- government spending.

Exogenous are variables that influence the outcome of a model decision. And their change is called autonomous.

The concept of endogenous variables

They are the outcome of the decision, determined in the course of the calculations according to the model. Endogenous variables are formed within the macroeconomic model. Therefore, they are called internal.

Endogenous variables are dependent on external conditions. Their role in the models is played by:

- level of employment and unemployment;

- output and economic growth;

- level of foreign economic activity;

- level of prices and inflation.

If we talk about the relationship of internal and external variables, then between them there are only one-sided causal relationships. Exogenous variables are factors that determine endogenous, but they themselves do not fall under their influence.