In order to understand the graph and the isocost map, it is worth knowing more than one definition. This will help to learn to understand such a difficult science as microeconomics.

What is an isocost?

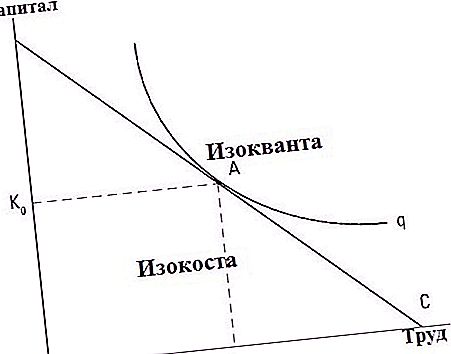

An isocost is a line that indicates a selection of resources, the use of which requires an equal amount of cost. It allows you to optimize profits at certain costs. On the graph, L is the labor factor, K is capital.

Properties of isocosts

The properties of the isocost are similar to the budget constraint line. It has a negative slope, the degree of which is determined by its equation. The slope of the isocosts on the graph also depends on the price ratio of factors of production. The location of the isocosts depends on the income level of the enterprise.

The isocost equation is C = Px * X + Py * Y. Here C is the cost, Px and Py is the price of the resources.

An isocost map is an image of two parallel lines that also have a negative slope. Indicates theoretically possible resource samples that provide the company with appropriate output volumes.

An increase in production capital or a decrease in prices for resources (material, natural, labor, financial) shifts the isocost to the right according to the schedule, and a decrease in the budget or a rise in prices to the left.

The schedule determines the most favorable for a given level of the economy of the enterprise selection of a combination of factors.

If you combine the isocost and isoquant plots, the conclusion suggests itself which way the manufacturer will choose to produce the volume of products he needs.

Isoquant is an infinite number of options for combining factors of production that provide the same amount of output. The optimal selection of resources for the manufacturer, providing the lowest cost threshold, is at the point of contact between isoquants and isocosts. This is called cost minimization. That is, in order to determine the optimal position for the company, you need to connect these two lines. The optimum point shows the minimum cost of a combination of production factors that will be used to produce the right amount of product.

Isocosta. Production function

Production is the process of using resources, including human resources. The purpose of production is to satisfy consumer demand for tangible and intangible goods.

The theory of material production describes the process of using production resources for processing into a final product.

By combining all factors of production, the final good is created for production and non-production consumption and accumulation.

The outcome of any enterprise depends on the efficient use of production factors. This is what the production function reflects, characterizing the dependence of the volume of the finished product on the amount of resources expended.

The production function is the interdependence between the volume of output and the cash costs of acquiring production factors.

Q = f (K; L)

Q is the maximum output of the product;

K, L - the cost of acquiring labor (L) and capital (K).

Q = f (K; L; M)

M - the cost of acquiring raw materials.

Q = f (kK α; L β; M γ)

k is the scale factor;

α, β, γ - elasticity coefficients.

Q = f (kK α; L β; M γ … E)

E - factor of scientific and technological progress.

α + β + γ = 1%

α = 1%; β, γ = const

α, β, γ - elasticity coefficients, which show how Q will change with a change of α + β + γ = 1%.

k - characterizes how proportional the costs of acquiring production factors are.

This production function allows you to identify the main properties of production factors:

- interchangeability - the production process is possible in the presence of all factors of production;

- complementarity.

The final result of production depends on the chosen combination of factors of production.

There is a limit to the growth of Q, provided that one factor of production is a constant value, and the second is a variable.

Q = f (K; L)

Q = f (x; y)

Q = ↑

x is the variable, y-const.

This situation is called the law of diminishing productivity or the law of diminishing returns.

Costs

To determine ways to minimize costs, you need to have an idea of what it is and what types of costs exist. What is an isocost of costs?

Economic costs are the cost expression of the resources or factors of production used in the production process. They are of an alternative nature, that is, each resource or factor of production involves multivariate use.

Cost types

Costs (costs) can be both explicit and implicit. Explicit - the costs involved in the production process (for the purchase of raw materials, components, electricity, wages for workers, depreciation, etc.)

Implicit costs are costs that are indirectly involved in the production process - rent, advertising costs, etc.

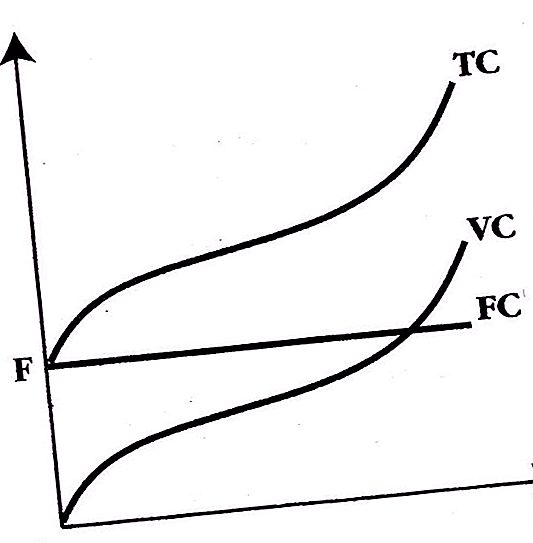

In the short term, the following types of costs are distinguished:

- permanent (are implicit) - FC (example - insurance premiums, equipment maintenance costs);

- variables (directly involved in the production process) - VC;

- general - TC - all costs.

The total costs are equal to the sum of the variable and fixed costs - TC = FC + VC.

According to the schedule: C - costs, Q - volume of production.

In the formation of total costs, variable costs are of particular importance.

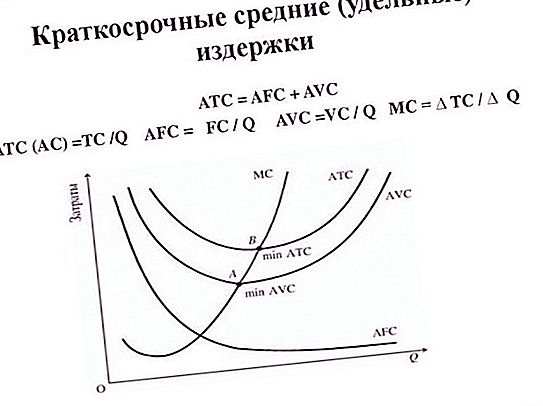

When making management decisions, average costs are especially important. This type of cost involves the calculation per unit of output, that is, average values.

Marginal Costs (MC) show the change in total costs as a result of a change in volume.

Marginal revenue (MR) shows changes in income generation as a result of volume changes.